DENVER — Rising homeowners insurance costs are becoming a new challenge for Colorado homeowners and buyers, adding pressure to an already-expensive housing market.

People shopping for a home usually focus on location, price and interest rates. Now, experts say insurance premiums are playing a much bigger role in the homeowning process. Colorado Chamber of Commerce President and CEO Loren Furman said the state is facing growing affordability challenges on multiple fronts.

“We’re also the fourth most expensive state for property and casualty insurance,” Furman said.

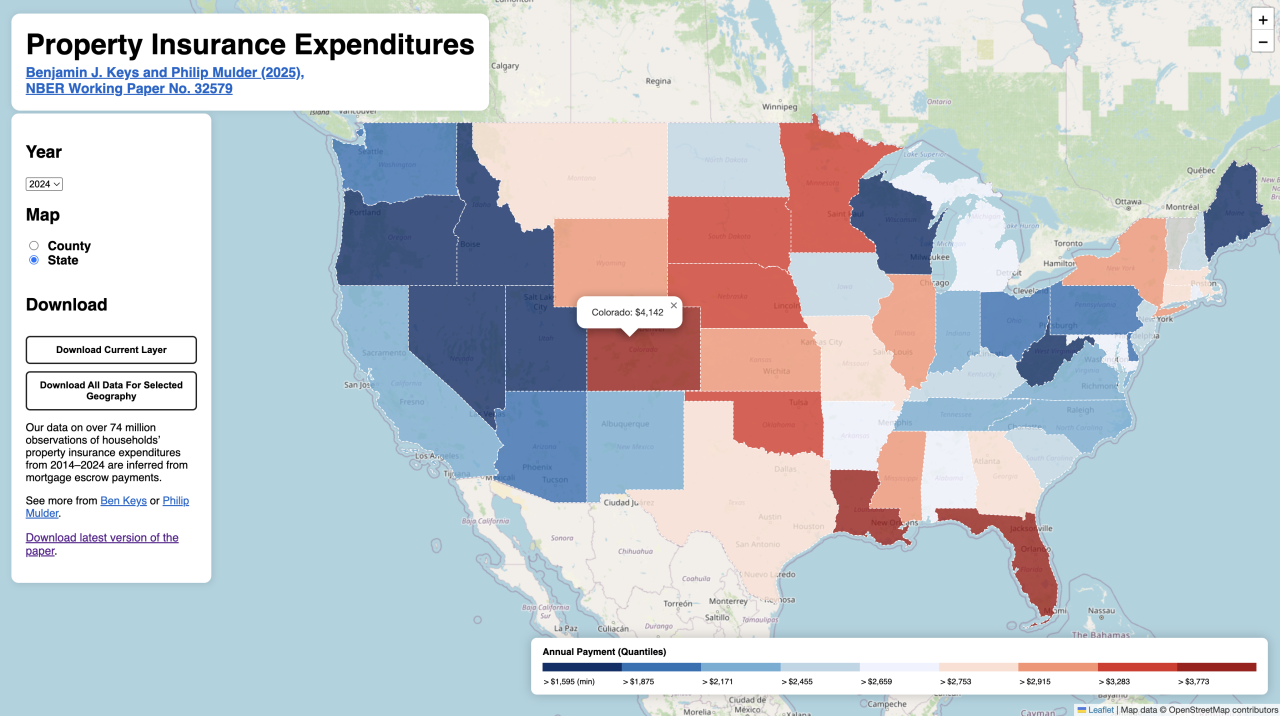

According to the National Bureau of Economic Research, the average homeowners insurance premium in Colorado is now about $4,100 a year — that’s a 137% increase over the past decade. Industry leaders say Colorado’s unique risk profile is a major reason why.

“One of the biggest cost drivers is hail and wildfire risk,” Furman said.

Those rising insurance costs are hitting at a time when home prices remain high. Furman said the Colorado Association of REALTORS reports the average home price in the state is now around $700,000 and has continued to rise year after year.

That combination is changing how buyers and sellers approach the market.

Cooper Thayer, a Denver-based real estate broker and market spokesperson for the Colorado Association of REALTORS, said homeowners insurance has become a regular part of affordability conversations.

“Homeowners insurance costs come up quite a bit, especially for buyers who are more budget constrained,” Thayer said. “Everything in housing comes down to monthly payments.”

Thayer said higher insurance premiums can force buyers to lower their price range or change what type of home they’re looking for. In some cases, sellers are also adjusting asking prices to account for higher ownership costs, including insurance, HOA fees and property taxes.

“In turn, sellers have had to adjust their asking prices to compensate for some of these increased costs,” Thayer said.

Experts say there are steps homeowners and buyers can take to help ease the burden. One solution involves making homes more resilient to damage.

“If we make homes more resilient to hail, especially our roofs and our windows, we can reduce the number of claims and reduce our overall aggregate premiums,” Thayer said.

Shopping around for insurance and reassessing coverage regularly can also help, though Thayer cautioned those steps alone won’t solve the problem.

“It’s not the solution that will fix everything, but it’s certainly a step in the right direction,” he said.

At the state level, Furman said the Colorado Chamber is backing proposals aimed at mitigation and long-term cost reduction. Those include funding for impact-resistant roofing, wildfire mitigation efforts and tax incentives to help homeowners pay for upgrades that reduce risk.

As Colorado continues to grow and climate risks increase, experts say homeowners insurance will play an even bigger role in housing affordability. While solutions are being discussed, Thayer said it will take time.

“We do have some solutions in the works,” he said. “But it has a long road ahead. It’s an uphill battle.”